As we end the year and begin a new one, what can we say was the most important health-related story of 2024, and what will be the biggest in 2025? Certainly, late in 2024 a huge story was the murder of Brian Thompson on the streets of New York. This was not in any way a random killing, but an assassination of someone the killer believed was responsible for hundreds or thousands of deaths in his role as CEO of UnitedHealthCare, the nation’s largest health insurer. As I discussed in my December 8, 2024 post ‘Murder of a Health Insurance CEO: People HATE the companies and the people who run them’, Thompson was guilty of presiding over a company whose role was to make money by collecting premiums and denying care. He also was guilty of having made this problem worse by bring in artificial intelligence algorithms, which had been shown to be wrong up to 90% of the time, to deny health care to his supposed customers – I say “supposed” because the only customers health insurance companies really have is their stockholders; the people they insure could be called “victims”.

Another huge story, which will become even bigger in 2025, is the planned nomination by President-elect Donald Trump of profound enemies of public health to the positions responsible for ensuring that health. Foremost among these, of course, is Robert Kennedy, Jr. to be Secretary of Health and Human Services. Kennedy is well-known as a vaccine “skeptic”, which essentially means vaccine opponent, and if he is confirmed as Secretary and is able to implement policies reflecting the positions he has long advocated, we will see the resurgence of many diseases long gone from American life with accompanying deaths, as I discussed on November 15, 2024 in ‘Raw milk, vaccines, and RFK, Jr: Some dates worth remembering’. Remember polio? Measles? I do, but most do not. Check out the numbers on this picture. This is an incredible threat to the public’s health.

But, ultimately, the real story of 2024 – and probably 2025, and sadly beyond – is the fact that the American people remain the only ones in the developed, rich or really even middle-income, world that do not have universal health insurance or care. This is what would prevent the crises, delays, denials, and deaths that the private health insurance industry heaps upon our population and that engenders the wrath of so many. Indeed, that wrath continues to grow because the people who are affected, either personally or through someone they love such as a family member, who realize the inexcusable evil that the actions of these companies inflict, grows over time. While only a small percent of the ostensibly insured will have a terrible event each year, with more years more people and families experience such terrible events. Also, of course, the practices of the health insurance companies become more restrictive and more draconian, leading to both more delays and denials and deaths and more out-of-pocket costs for more people. In other countries, this happens, essentially, very little or not at all. The following chart presents the dates when other countries implemented universal health care, and when they got rid of it because it wasn’t working. Look at it carefully and you might discern a trend:

The US has a higher mortality rate than many of these countries. Jim Kahn, in the Health Justice Monitor, makes an effort to quantify the extent to which health insurance (or lack of it) contributes to this. It is an estimate, but as he notes, whether 170,000 or 220,000, it is too much. And, more, we spend much more than all these other countries on what we call “healthcare” despite so much of it going to corporate profit, that the fact that there is any excess mortality due to lack of health insurance is even more intolerable.

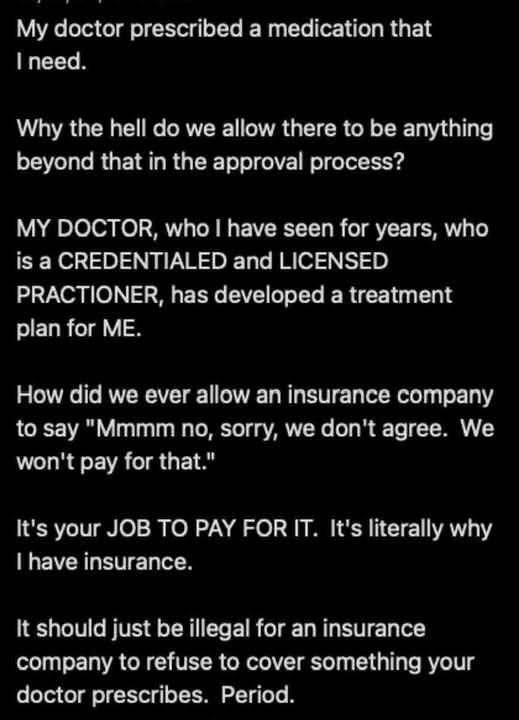

This might come as a shock to many Americans, especially those who have yet to personally experience the delays, denials, and deaths that the for-profit health insurance industry heaps upon its victims, because we are regularly and consistently told by politicians and pundits that a universal health insurance system would be a bad idea, that it wouldn’t work for Americans. That it would be too costly. That it would limit our freedom. We need to recognize that this is not true. Few of us want to have the freedom to choose which insurance company takes our money and then tries its best to limit our access to care (although, if we can afford it, we might choose the one that does it least). What we do want is the freedom to choose the doctors and hospitals that we believe will provide us the best care for our health needs and have our insurance pay for it. Of course, this is not the freedom that they are talking about; what they mean is the freedom of insurance companies (and to be fair, many health care providers) to make as much money as possible, which is what would be limited in a universal government-run health insurance system. And, oh, by the way, provide the funds to pay for it. Imagine that our health care dollars, from our pockets and those of our employers and our government (from the taxes we pay; the large corporations and billionaires who own them don’t) could be spent on providing us with health care rather than lining corporate pockets!

There are actual examples of “single payer” health care in the US. Military retirees and families are covered by government-funded health insurance through the VA or TriCare. In the military itself, for active duty service members, health care is not only single-payer, it is government run. The other big example of single-payer available to Americans is traditional Medicare, for those over 65 or disabled. Medicare. The most popular government program since…Social Security. Under traditional Medicare, health care services are approved for people who need them and have them ordered by a doctor, not micromanaged for each individual with people (or AI!) denying them willy-nilly. In an alternative to Medicare, people can opt for enrollment in an HMO/PPO like system run by the same insurance companies that insured (and often screwed) them before they became eligible for Medicare, and have it paid for by Medicare funds. This program, misnamed “Medicare Advantage”, takes away the guarantees of traditional Medicare and puts you back a the mercy of those for-profit health insurance companies that have treated you so well before!

This is exactly what we don’t need – erosion of Medicare. We need Medicare to be improved, to pay for 100% of all needed medical care, and expanded to cover every American, cradle to grave, paid for by the money now going to insurance company and pharmaceutical and device company and health system profits. The reason to do it is because it would benefit people, remove the major cause of heartache, loss and bankruptcy in the US, and make us more secure and happy people. The reason not to do it is that these huge corporations would no longer be making their exorbitant profits by taking premiums and denying health care, and thus would not be able to make such large contributions to the legislators who should be acting, instead, for the American people.

What do you want? Maybe in 2025 it is time to let your legislators know!

A final thought from Bernie Sanders: