Are health insurance companies the real enemy of Americans’

health? A strong argument can, and has been, made by myself and others that they

are. More broadly, however, the enemy is all the companies that pursue making money

as their primary goal, with providing healthcare a sideline (albeit a costly

one). So many corporations are involved and responsible that it is hard to be

sure that insurance companies are the main ones at fault. “Even” actual health

care providers – mainly hospitals and “health systems” – try to squeeze out the

poor and poorly insured and greatly prefer to deliver only the most high-profit-margin

care. And, certainly, one cannot leave out the drug companies, making gigantic

profits at the cost of our health (they remain #1 in profits, every year), or

the less-well-known but also very dangerous “PBMs”, pharmacy benefit managers,

who bundle our drug plans, and act as middlemen between the insurers and the

drug companies and the providers. (You notice I didn’t say “consumer” or “patient”;

they are no more than grist for the profit mill!)

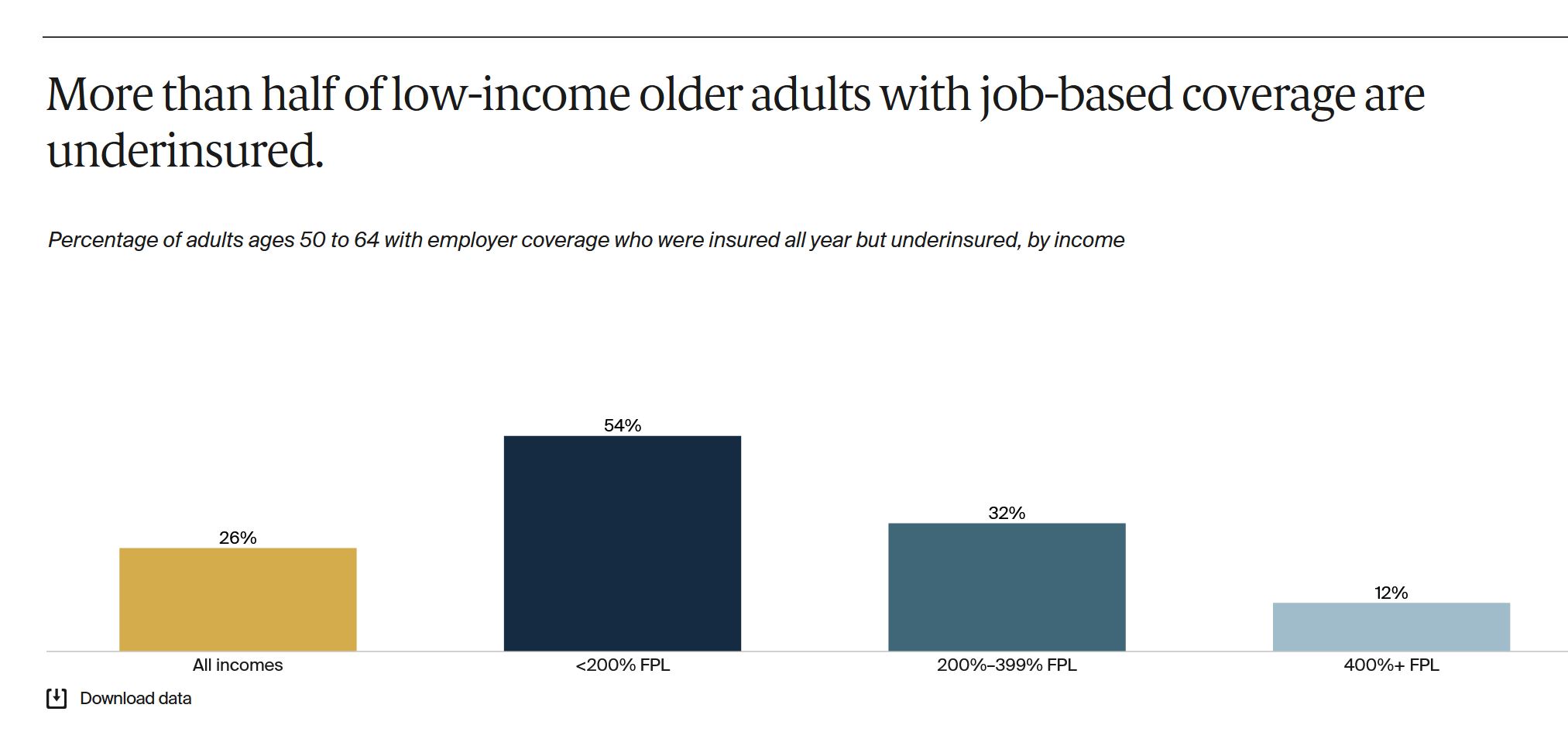

But one can still make a strong case for insurance companies being at least a major cornerstone of the evil empire, sucking money out of government coffers, employer contributions, and, yes, your pockets, for the privilege of denying you care and padding their bottom lines. Long noted for their unwillingness to cover everyone, the insurance industry is moving the needle by providing poor coverage even to those it does insure. Two recent studies have looked at the financial burden on older adults provided by health care, one at those with private insurance and the other at those with Medicare.

The Commonwealth Fund looked at the coverage and costs for

older-but-not-yet-Medicare adults 50-64 in ‘Can Older Adults with Employer Coverage Afford Their Health

Care?’ by Lauren A. Hayes and Sara R. Collins (August 10, 2023). A majority

of these folks have private insurance through their employers (55%) with higher

income (>400% of the Federal Poverty Level, FPL) at 82% and low income

(<200% FPL) at 22%. It wasn’t enough. More than half of low-income and more

than 1/3 of middle income (200-400% FPL) people had difficulty paying their

premiums and didn’t get adequate medical care because of the cost.

Unsurprisingly, those worst affected were not only low-income but sick; the

issue of paying for health care is greatest when one has health problems.

The Kaiser Family Foundation study, ‘Medicare Households Spend More on Health Care Than Other Households’, by Nancy Ochieng, Juliette Cubanski, & Anthony Damico (July 19, 2023) examined adults over 65, those on Medicare. They found – well, what the title says. Again, not surprising; older people are sicker, and sicker people use more healthcare (duh!) and it costs them more. While Medicare is a federal government program, there are still out-of-pocket costs associated with it. For hospital care (Medicare Part A, funded by your paycheck deduction), traditional Medicare (TM) pays only 80% of approved charges, which means sick Medicare recipients have to come up with the other 20% (which can be a huge amount of money) or have a Medicare-supplement policy to cover it, which of course costs additional premiums. Medicare recipients also have to pay a monthly fee for Medicare “Part B” (the “outpatient” portion) which usually is deducted from their Social Security payments. At least this is tiered, so higher income people pay more and lower income less (or sometimes nothing). Also they have to pay for a drug plan (Part D).

About half of Medicare recipients are now in “Medicare Advantage” (MA) plans, which are essentially HMOs. I have written about them previously, but because they are not actually Medicare (although paid for with Medicare dollars) but private insurance, they have the ability to deny coverage altogether. They have good perks if you don’t need expensive care (often no co-pays, no 20% coinsurance, drug coverage so no need for a separate Part D plan, coverage for some things TM doesn’t cover like glasses and hearing aids) which make them attractive to healthier seniors. But while TM covers (if only at 80%) the things it says it covers, and doesn’t deny individuals, MA can and does. So while Medicare Advantage can be advantageous for some seniors, its greatest advantage is to the insurance companies.

Indeed, that some people are better off with one type of plan and others with a different one is both understandable and OK. But that the difference is whether you are sick or not is dangerous, since the non-sick can quickly become sick, especially if they are elderly. That we try to segment public opinion by pitting the sick against the not-yet-sick (“I’m doing ok, and can afford my premiums and healthcare, for now”) is what is truly sick, and intolerable. It is a marker of a reprehensibly designed system.

The authors of the Commonwealth Fund report have a number of

suggestions for addressing the problems that they identify, all of which are

tweaks to our current system, and, in the unlikely event that they were

implemented, would immediately be “gamed” by the power players – the insurance

companies and the health systems – to ensure that there would still be lots of

people left out, lots of people suffering. Their suggestions do not entail

scrapping the entire for-profit insurance system that strangles the health of

our people in favor of an adequately-funded single payer system, but rather the

creation of new programs, and new rules to try to limit the damage

caused to the health of older Americans by a system that simply should not

exist

Seniors can be attracted to MA plans because of the costs TM doesn’t cover, especially the 20% of hospital bills. Those in MA plans, as well as those “younger” – still employed – older people in employer-based insurance plans can be financially screwed because those plans are operating with the goal of making money for the companies, not ensuring health care. The fact is that both problems could be addressed together – by getting rid of the profits and costs of insurance companies, enough money could be saved to cover 100% of all health care needs for Medicare recipients. One could say this is “ironic”, if it weren’t for the fact that irony implies lack of intentionality, and this criminally flawed and abusive system is clearly intentionally structured.

Dr. Don McCanne, who reported on this in his recent “Health Justice Monitor”, writes

“Should

that be the primary mission of our health care administrators? Of course not!

Their primary mission should be to move health care to the people, the

patients, all of the patients, and they need to use our health care dollars to

do that. Our current system has demonstrated beyond any doubt whatsoever that

private administrators have been and always will be on the wrong mission, and

we need to replace them with public administrators who will always pursue a

mission for the public good.”

Yes. Stop trying to make deals with the devil. Those companies, including insurance companies, taking money intended to provide healthcare as salaries and profit are evil, and it is hard to think of the legislators and executive-branch functionaries who facilitate and enable this as anything else.

Our government should use its (ie, our) money to fund our promises for healthcare to our seniors, not insurance companies who pay them back with graft.