“Mr.

McConnell has always taken pride in protecting his members.” -- NY Times, June 23, 2017

First, let’s start with a reminder about how insurance

works. Money (“premiums”) is collected from everyone, or as many people as

possible, and when the bad thing happens (insurance is almost always about

protecting against bad things, like car accidents, or fires, or death, or

illness), the victims are compensated. If it pays out more than it collects,

then the insurance company goes bankrupt and can no longer pay out. This works

for all types of insurance, whether for-profit (as most is in the US),

not-for-profit (like many health-insurance companies in other countries), or

social insurance where everyone is a client and government is the insurer.

Insurance companies, especially for-profit insurance companies, have to build

in a profit margin as well. In addition, they prefer insure people who are at

low risk of requiring payout, and not to insure or charge higher premiums to

those who are at higher risk (e.g., younger drivers, for car insurance). This

process is known as “underwriting”.

If an insurance company is forced to insure a lot of high-risk

people (as they were under ACA) and can’t charge them really a lot (under ACA they could charge 3 times as much), they

need a lot of low-risk people to pay premiums to be able to fund their probable

payouts; thus the “individual mandate”. For social insurance, such as

government financed health insurance programs (as in many other developed

countries, or Medicare and Federal employee and military programs in the US),

it is actually not necessary that more money come in from premiums than is paid

out, because the government can (if it wishes) subsidize the loss from other

funds. This is, of course, a political decision on how to allocate tax dollars

and how many tax dollars to collect.

The Senate Republican

leadership has made its position on this completely clear with its recently

unveiled “health care” bill, the “Better Health Care Act” (BHCA). Crafted by

Majority Leader McConnell and a small group of white men from a small group of

places (for example, 2 senators each from Utah, Wyoming, and Texas). It will and

should be called #Trumpcare; while the President didn’t write it, he has

endorsed it and will sign it if it passes the Senate and the House

reconciliation. It is clearly a tax-cut-for-the-wealthy bill that derives

funding from the reduction (and sometimes elimination) of health care coverage

for a very large percent of Americans; this is detailed by the NY Times’ Margot Sanger-Katz in “Shifting

Dollars From Poor to Rich Is a Key Part of the Senate Health Bill”, June

22, 2017. The Times also has a piece

by Sanger-Katz and Haeyoun Park that contains a clear listing of what will be

cut from the ACA in order to fund these tax cuts, “How

Senate Republicans plan to dismantle Obamacare”, summarized in the graphic.

However, the details are important; even the parts of the ACA that the BHCA “keeps”

are largely undercut by other parts of the bill. For example, it keeps the

requirement that insurers must issue policies to people with pre-existing conditions (which can range from heart

disease and cancer to endometriosis and broken bones and everything else),

which is good. But it raises the amount that insurers can charge these people

from 3 times as much under ACA to 5 times as much. This is a big deal, and a

bad deal, for people with disabilities and for older people who are, (surprise!),

much more likely to have pre-existing conditions.

The Senate Republican

leadership has made its position on this completely clear with its recently

unveiled “health care” bill, the “Better Health Care Act” (BHCA). Crafted by

Majority Leader McConnell and a small group of white men from a small group of

places (for example, 2 senators each from Utah, Wyoming, and Texas). It will and

should be called #Trumpcare; while the President didn’t write it, he has

endorsed it and will sign it if it passes the Senate and the House

reconciliation. It is clearly a tax-cut-for-the-wealthy bill that derives

funding from the reduction (and sometimes elimination) of health care coverage

for a very large percent of Americans; this is detailed by the NY Times’ Margot Sanger-Katz in “Shifting

Dollars From Poor to Rich Is a Key Part of the Senate Health Bill”, June

22, 2017. The Times also has a piece

by Sanger-Katz and Haeyoun Park that contains a clear listing of what will be

cut from the ACA in order to fund these tax cuts, “How

Senate Republicans plan to dismantle Obamacare”, summarized in the graphic.

However, the details are important; even the parts of the ACA that the BHCA “keeps”

are largely undercut by other parts of the bill. For example, it keeps the

requirement that insurers must issue policies to people with pre-existing conditions (which can range from heart

disease and cancer to endometriosis and broken bones and everything else),

which is good. But it raises the amount that insurers can charge these people

from 3 times as much under ACA to 5 times as much. This is a big deal, and a

bad deal, for people with disabilities and for older people who are, (surprise!),

much more likely to have pre-existing conditions.

While BHCA (Trumpcare) repeals the individual mandate, which

will make some people happy (until they get sick) and the employer mandate

(which will make employers happy), it also repeals the subsidies for

out-of-pocket costs and decreases funding for subsidies to make policies on the

exchanges affordable. The new bill would make either premiums or deductibles

(or both) unaffordable for many Americans. It limits and sometimes eliminates

the requirement that insurers provide “essential health benefits”, like

preventive care and contraception, allows insurers to set annual and lifetime

limits on how much they have to pay, and makes major negative changes to

Medicaid. Medicaid is currently largely paid for by the federal government,

50%-80+% depending on the average state income, and 90-100% for people covered

by Medicaid expansion. The “changes” include (gradually, so the impact won’t be

seen for the 2018 election) cutting and capping the amount the federal

government pays, shifting costs to the states, which often will not be able (or

willing) to cover them.

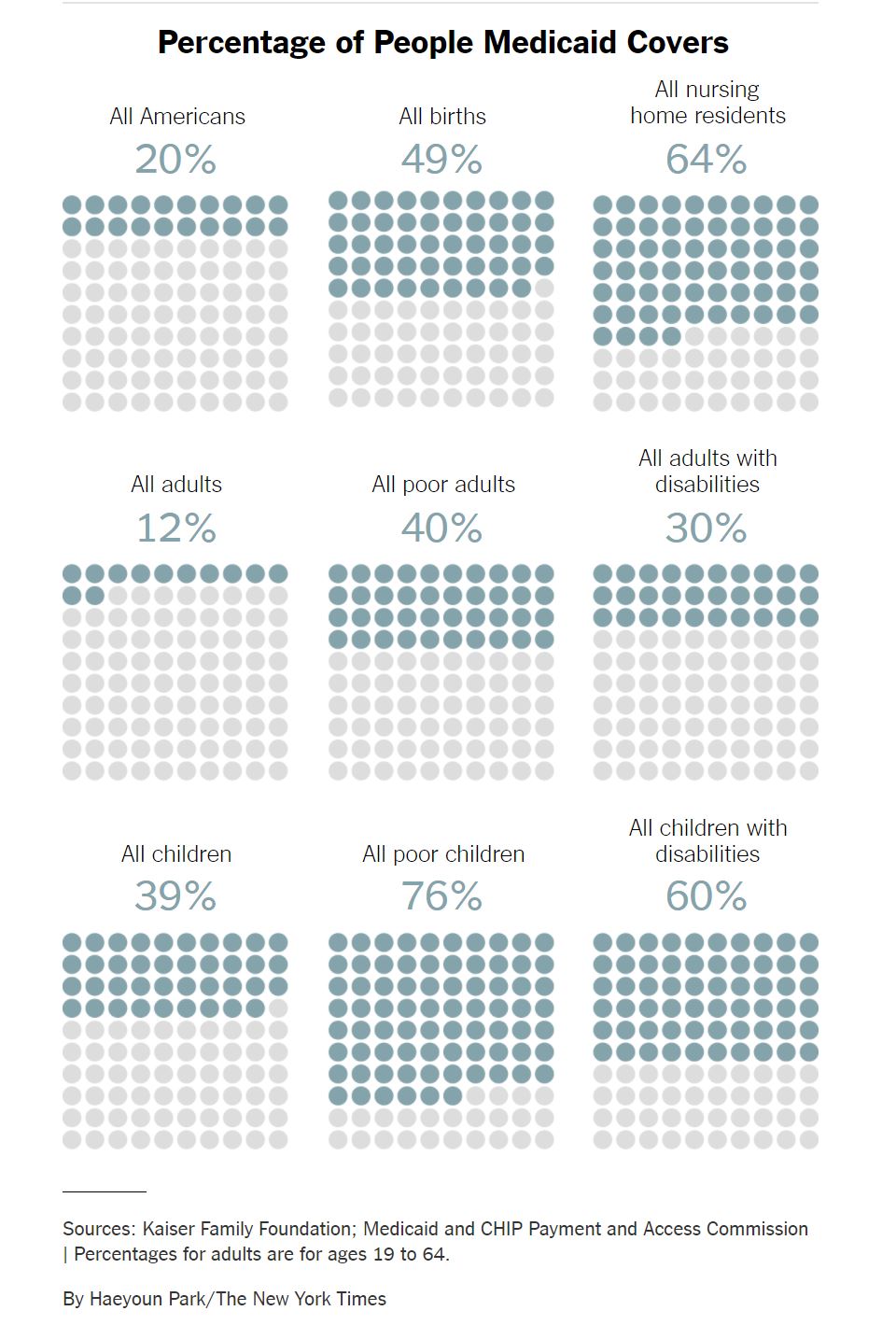

This will affect a lot of people. Medicaid is now the

largest insurer in the US, covering 69 million Americans, even though many

states did not expand it under the ACA to cover poor adults. What it does is

summarized in “How

Medicaid works and who it covers” by Abby Goodnough and Kate Zernike. It

covers, as seen in the accompanying chart, 79% of poor children (and more than a

third of ALL children), 64% of nursing home patients (many of whom were middle

class before the NH wiped out their savings!), 60% of children with disabilities,

49% of births, 30% of adults with disabilities. The people who will suffer from Medicaid cuts are old people in nursing

homes, children, and disabled people (many of whom are able to stay in the community

and even keep jobs rather than being in nursing homes because of this support). With

the caps on lifetime benefits, it means, as

Dr. Eve Shapiro points out in an Op-Ed in the Arizona Daily Star, “that a premature baby on private insurance

could exceed her lifetime limit on coverage before she even leaves the hospital”!

And, with the right convergence of decisions by the state, the same could happen

to an infant with Medicaid.

This is a big deal. Ideologues and pundits and politicians like

to debate theoretical issue to see who scores the most points. They want to be

the “most conservative”, the most “anti-abortion”, the most “pro-industry”, the

most “anti-tax”. If they are articulate they may think that making their smarmy

points makes them win. And I guess it does. Except the losers are not those on

the other side of a debate podium, they are the majority of the American

people, the politicians’ constituents, who don’t get treatments, don’t get

diagnosed, do get sick and die. Lives, not ideologies, are at stake.

Except, of course, it is about ideology. This is made clear

in “A

debate that shows what each party cares about” by Neil Irwin the Times. No one, certainly not a senator

who has to run for re-election, wants to say that they are about making it

harder or impossible for many (often the majority) of their constituents to be

able to access health care, or to pay for it, or to get the treatments and

therapies they need. But make no mistake: every senator who votes for this bill

is saying exactly that, that they value tax cuts for the most privileged above

basic health care for the rest of us. “This plan will improve the affordability

of health insurance,” lied Sen. McConnell in a recent

opinion piece in the Cincinnati paper.

Yes, “Mr. McConnell

has always taken pride in protecting his members.” And his donors. It is

too bad that he has no interest in protecting the rest of us.

No comments:

Post a Comment